News

FX Overlay with a clear goal: Raise returns, reduce currency risks

Date:

11. December 2023

- Portfolio Management

With the end of the global era of low interest rates and amid significant geopolitical tensions, currencies have also been experiencing sharp fluctuations. Professionals responsible for managing portfolios must now, more than ever, keep a close eye on currency risks. It is crucial to keep costs as low as possible in FX Overlay. With Universal Investment, institutional

Higher interest rates and geopolitical turbulence across the globe: against this backdrop, certain unforeseeable decisions by central banks and political developments may continue to contribute to currency volatility in the near future.

Institutional investors got a foretaste last year and this year that not only emerging market currencies are affected, but also key G10 currencies. The US dollar appreciated by 19 percent against the euro at times, initially a development that benefited euro investors with US dollar exposure. However, the pendulum can swing just as quickly in the other direction: this was followed by a depreciation of the US dollar against the euro by about 15 percent. Fluctuations of 20 percent within a few months pose a risk that is increasingly untenable in professional portfolio management. The demand for currency hedging is growing – and not only among investors such as pension funds who are already limited in their ability to take on foreign currency risks in their portfolios due to regulatory requirements.

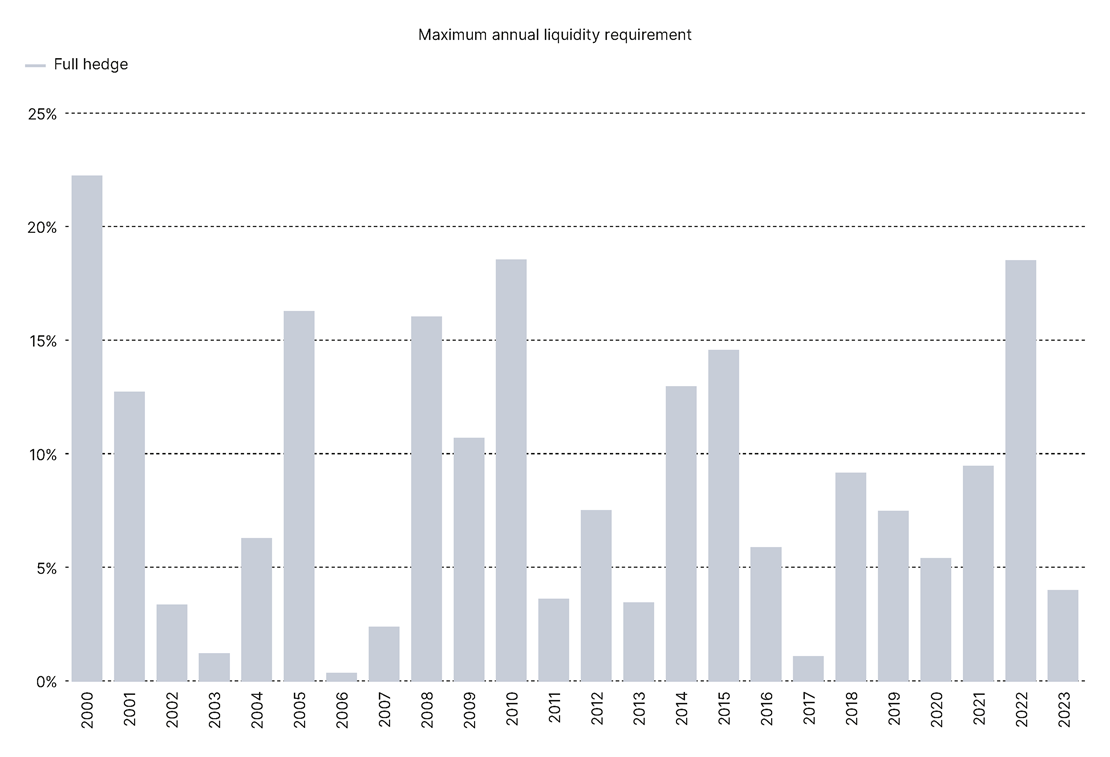

Liquidity requirements and carry costs of static currency hedges

As desirable as it is, currency hedging does not come for free. Especially in highly volatile markets, there can be significant liquidity requirements if full hedging requires a substantial margin deposit. In the year 2022, a peak of 19 percent was recorded for hedging a US dollar exposure in euros. As this meant that investors needed to deposit almost 20 percent of assets as liquid collateral, the opportunity costs for a fully hedging FX overlay were notably high.

High opportunity costs:

liquidity requirements for static fully hedging overlays

Liquidity requirement for a US dollar hedge for euro investors. Source: Universal-Investment-Luxembourg S.A., as per 31.10.2023

Liquidity requirement for a US dollar hedge for euro investors. Source: Universal-Investment-Luxembourg S.A., as per 31.10.2023 Another factor that often leads to negative returns for euro investors is the carry costs. These arise from the difference between interest rates in the US and the eurozone. Often, higher interest rates are paid in the US than in Europe. This also affects the FX forwards used for currency hedging, which continuously lose value. As a result, the carry incurs costs at all times, even if the euro-dollar exchange rate remains stable and hedging is not utilised. Carry costs vary over time: between 2010 and 2023, they reached up to an annual 3.5 percent!

Currency hedging becomes increasingly important for investors in volatile times – but full hedging incurs costs. Our FX OverlayPLUS, on the other hand, can help improve performance.

Dynamic FX OverlayPLUS - the goal: only use when necessary

It is difficult to reduce the aforementioned costs using classic static overlays. However Universal Investment offers an innovative and transparent rule-based solution through its dynamic FX OverlayPLUS.

This approach utilises tactical signals, enabling exploitation of opportunities by, for example, temporarily reducing hedging levels and costs if hedging is not required. The basis for this are the signals that the FX OverlayPLUS obtains, for example, although not exclusively, from Universal Investment's partner Vescore. Universal Investment’s successful track record with Vescore and its Risk OverlayPLUS that manages equity and bond portfolio risks spans more than a decade.

The signals include the current valuation of a currency, macroeconomic factors, and the prevailing trend. In the FX OverlayPLUS, these signals are deliberately embedded in a conservative manner, emphasizing value preservation. This means that the default state of the system is essentially a full hedge. Gradual reduction of the hedge occurs only if distinctly positive signals emerge.

Furthermore, there is an additional risk buffer. This is a dedicated FX risk budget that is bolstered by the profits from the currency portfolio (and diminished by its losses). If the budget becomes too small and the risk buffer inadequate, the FX OverlayPLUS, independent of existing tactical signals, switches to hedging to consistently mitigate risk.

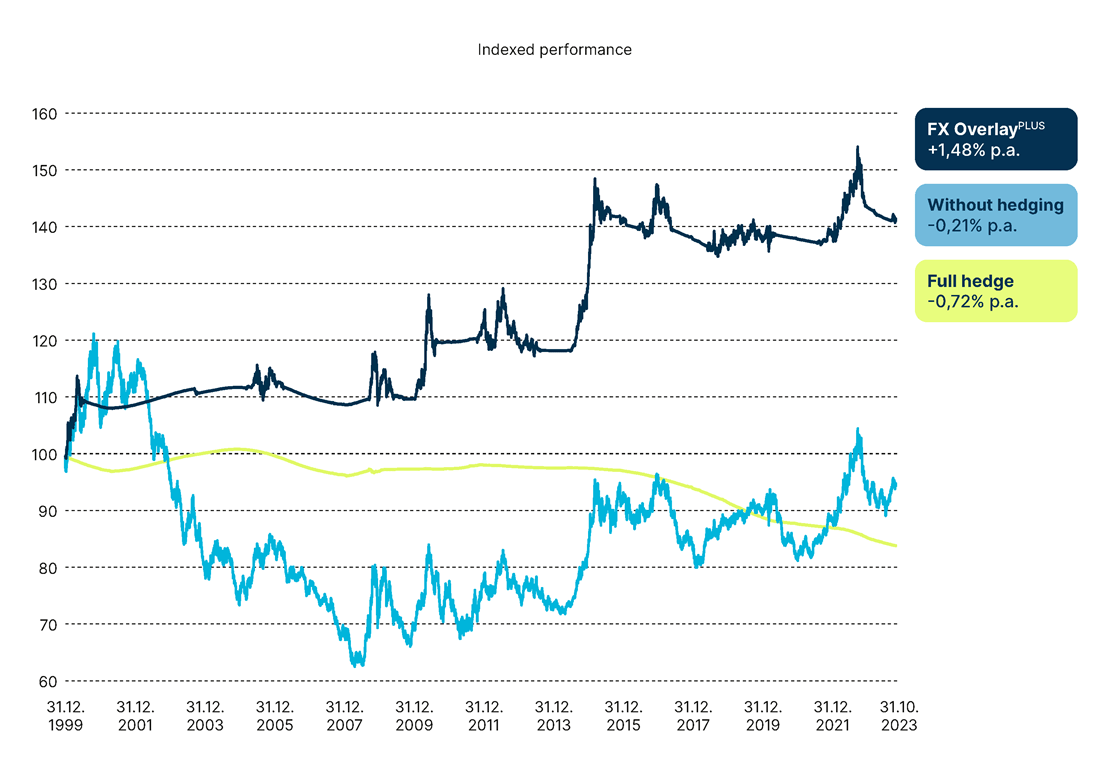

In our turbulent millennium, portfolio managers would have done well with this extremely conservative approach, as evidenced by backtests in the following chart. The chart illustrates the currency effects from the dollar portfolio for euro investors.

Improved performance through dynamic hedging with FX OverlayPLUS

Dates: Own calculation / results of the portfolio insurance concept in the context of a simulation study. Source: Universal-Investment-Luxembourg S.A., as per 31.10.2023

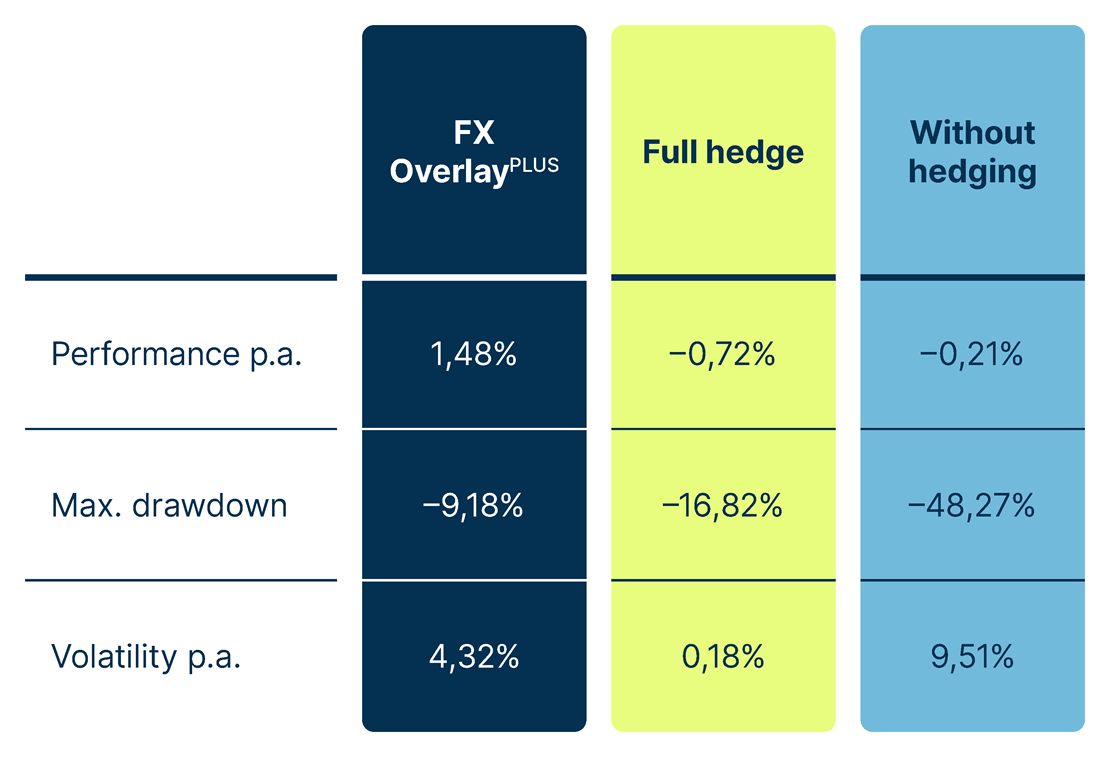

Dates: Own calculation / results of the portfolio insurance concept in the context of a simulation study. Source: Universal-Investment-Luxembourg S.A., as per 31.10.2023 The FX OverlayPLUS would have contributed a positive annual performance of 1.48 percent to the portfolio between 2000 and October 2023, while full hedging would have incurred annual costs of 0.72 percent. An unhedged US dollar portfolio would have suffered annual currency losses of 0.21 percent over the same period. The risk parameters compared to an unhedged portfolio are also favourable: With FX OverlayPLUS, the volatility in the observation period decreased by 55 percent and the maximum drawdown by 81 percent (see table).

FX OverlayPLUS: impressive figures since 2000

Source: Universal-Investment-Luxembourg S.A., review period 1.1.2000 to 31.10.2023

Source: Universal-Investment-Luxembourg S.A., review period 1.1.2000 to 31.10.2023

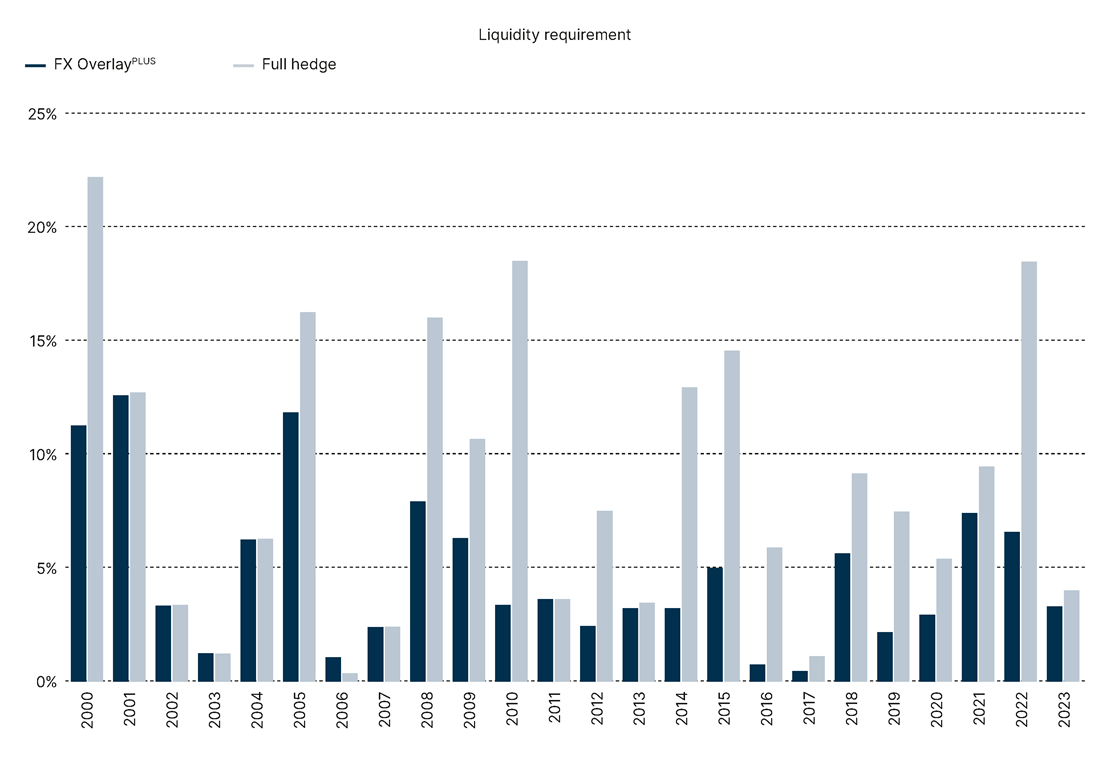

Compared to traditional full hedging, our dynamic FX OverlayPLUS can significantly reduce liquidity requirements and carry costs for currency hedging.

The opportunity costs of a currency overlay can also be significantly reduced through dynamisation using tactical signals. The FX OverlayPLUS distinguishes itself by unhedging in phases when hedging is unnecessary, resulting in significantly lower liquidity requirements compared to traditional full hedging.

Static versus dynamic hedging:

FX OverlayPLUS reduces liquidity requirements

Maximum liquidity requirement per year. Source: Universal-Investment-Luxembourg S.A., as of 31.10.2023

Maximum liquidity requirement per year. Source: Universal-Investment-Luxembourg S.A., as of 31.10.2023 On average, liquidity requirements were reduced by about 50 percent per year – meaning that with FX OverlayPLUS, a significantly larger portion of the assets under management would have been available for investment purposes.

Hedging of (currency) share classes: more market opportunities for asset managers

FX hedging can have a different function for asset managers than institutional investors. Asset managers generally pursue an investment idea and strategy aimed at achieving specific return targets.

Investors in different currency zones outside the fund's base currency might not achieve the asset manager’s objective if currency effects reduce the results of the base portfolio.

”This is where our NAV hedging, which is currently enjoying very strong demand, comes into play,” says Björn Allers. With the help of NAV hedging, share classes can be offered in different currencies that aim to closely replicate the performance of the main fund.

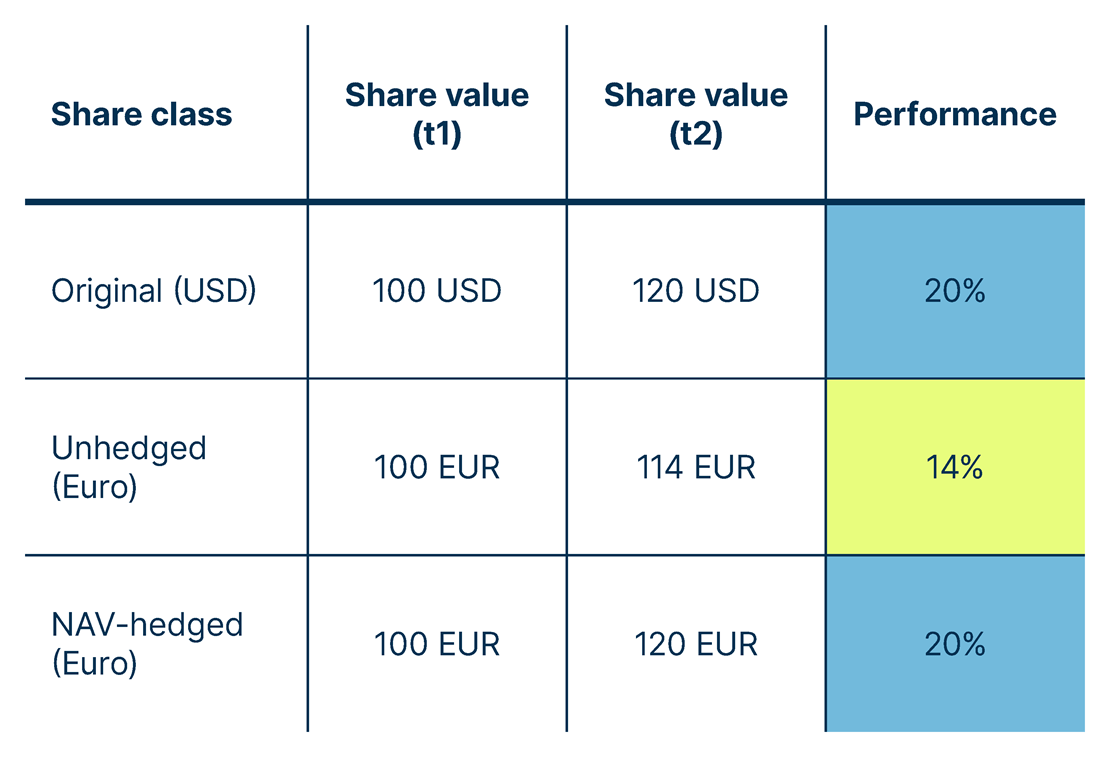

Example of NAV FX hedging effects

Hypothetical calculation example in the event of a devaluation of the US dollar against the euro between times t1 to t2 by five percent. Source: Universal-Investment-Luxembourg S.A.

Hypothetical calculation example in the event of a devaluation of the US dollar against the euro between times t1 to t2 by five percent. Source: Universal-Investment-Luxembourg S.A. The currency experts at Universal Investment hedge the NAV of the foreign currency share class using forwards or futures. This allows asset managers to make their investment ideas accessible to investors in other currency markets without compromise.

The FX hedging of share classes can contribute to opening new sales markets for successful fund concepts, as it allows for the explicit offering of shares in the respective currencies of these markets.

Portfolio hedging offers an alternative approach. This involves hedging the largest foreign currency positions of the portfolio against the fund currency. Asset managers can also use it to systematically tap into the potential returns of selected securities in the base portfolio, while avoiding the associated foreign currency risks.

FX overlay management: experience, scale, best execution

Universal Investment enjoys an excellent standing as a manager of currency risks in Europe. With more than 20 years of experience in portfolio management, the company currently manages assets totaling 27.1 billion euros in various FX mandates.

With the derivatives used, investors can choose between futures and forwards. The latter provides greater flexibility in terms of duration and nominal values. In addition, they can often offer more liquidity. Futures, on the other hand, as exchange-traded securities, do not require any additional collateral setup.

Universal Investment adopts a clear best-execution approach and, as a major manager, always receives multiple competing offers from banks and counterparties. This ensures the best price for clients in FX overlay management. Independent analyses of transaction costs consistently validate the results of this approach.

In addition to FX hedging of common liquid asset classes such as equities and bonds, Universal Investment's expertise also covers currency hedging of alternative investments with lower liquidity. This allows the company to offer currency hedging for complex portfolios of institutional investors. The challenge in hedging alternative investments often lies in the delayed availability of data. Victor Bemmann outlines Universal Investment's solution: “Backed by many years of experience, we have succeeded in aggregating the currency exposures from various sources, even in complex structures, and then managing them consistently.”

©2023. All rights reserved. This publication is exclusively intended for the use of professional and semiprofessional investors and is not intended for private investors. This publication is for marketing purposes only. The information provided should not be taken as recommendation or advice. All information is based on publicly available sources which we consider to be reliable. We cannot guarantee the accuracy or completeness of the information, and no statement in this publication is to be understood as such a guarantee. The opinions expressed in this publication are subject to change without notice. Information on historical performance do not allow conclusions about or otherwise guarantee future performance. The sole basis for the acquisition of units is the Fund documentation for the respective investment fund, which is available free of charge at Universal Investment and in the Internet at www.universal-investment.com. This does not constitute an offer or invitation to subscribe for units or shares of an investment fund. The information presented should not be considered reliable in this sense, as it is incomplete with regard to the possible interpretation as a subscription offer and may still be subject to change.